5paisa Research Team

5paisa Research Team

Sachin Gupta

Sachin Gupta

List Of Maharatna Companies In India

by

Tanushree Jaiswal

9th Jul 2024

It was 05th March 2020, when RBI took the control of India’s fifth largest private bank- Yes Bank. It took over the operations of the bank, halted the withdrawals by customers, and put the bank under a moratorium.

The action by the central bank spooked the investors as well as depositors of Yes Bank.

The problems with the bank first surfaced when RBI asked Rana Kapoor to step down as the CEO of the bank. Prior to this incident, Yes Bank was among the fastest-growing banks in India and was a sweetheart stock of most investors.

After the incident, credit rating agencies raised red flags on Yes Bank's exposure to risky loans.

All these incidences created uncertainty among the shareholders and they started selling their shares. In just one year the company’s share lost 90% of its value.

In March 2020, RBI finally decided to take the charge and appointed Prashant Kumar, who was then CFO and deputy managing director of SBI to look into the mess created by Rana Kapoor.

Prashant meticulously looked at the company’s books and found out that it was grossly under-reporting its bad loans. The company relentlessly gave out loans to corporate biggies, without having adequate deposits to back these loans. After the review, the company posted its biggest ever loss of more than Rs. 18,000 crores.

India's fifth largest private bank was on the verge of collapse. Its collapse would have had a dent in the economy So, RBI requested SBI and other banks to jointly take a 79% stake and save the bank from dying.

Fast forward to 2022, Prashant Kumar is the CEO of the bank and the company announced its first full year profit after the 2019 fiasco, and for a bank to turn profitable just two years after the biggest ever loss made in the history of Indian banks is commendable and we need to speak about it!

The company posted a profit of Rs.1066 crores in FY22 against a loss of Rs.3462 crores in FY 21.

In 2019, when RBI halted the withdrawals, customers lost faith in the bank. As soon as RBI lifted the restrictions, people started withdrawing their money. Now how do the withdrawals affect a bank?

In hindsight, a bank’s job is to raise money from different sources and lend that money to different individuals or organisations at a higher rate and profit from it. Simple.

Now, the profitability of the bank depends on its source of funds. If a bank raises money at a higher interest rate its margins will squeeze and profitability will take a hit.

Therefore, it is important for a bank to raise money at the lowest rate possible, other than borrowings a bank raises money in the form of deposits from customers. Traditionally, there are three ways in which the customer deposits money with a bank

Current Account: There is no interest paid on the current account.

Savings Account: An interest rate of 3 to 4% is paid on savings accounts.

Fixed Deposits: Money deposited in a fixed deposit earns a higher interest rate (6-7%) than savings deposits

Amongst all sources, Current account and Savings account deposits are the cheapest source of fund for any bank. That is why the analyst always speak of the CASA ratio while analysing a bank. The ratio basically tells you that of all deposits with the bank, how much is in the form of CASA. The higher the ratio, the lesser would be the cost of funds.

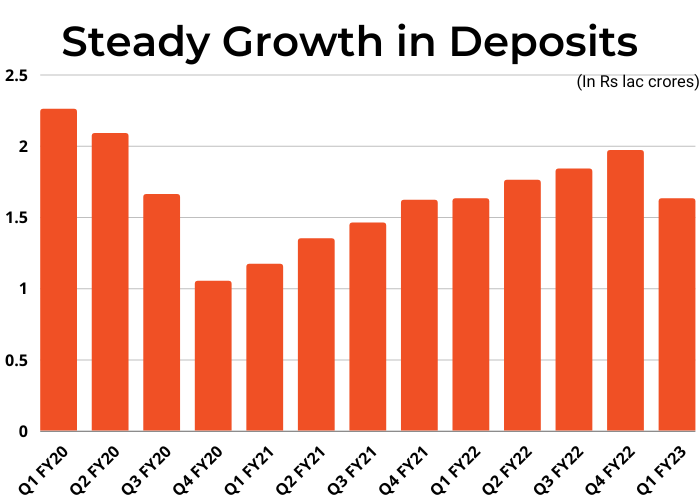

In 2019, when RBI halted the withdrawals of deposits from Yes Bank, it sent chills down the spine of people who had deposited money in the bank. They feared they would lose all of their money and hence customers relentlessly started withdrawing the money, due to which the CASA deposits with the bank started drying up.

The company’s deposits reached their peak in 2019 when they went to Rs. 2.27 lakh crore. Post the collapse, they went down to Rs. 1.05 lakh crore in March 2020. But now, just two years after the incident the deposits with the bank have doubled to 2 lakh crore. The bank’s deposit base has grown at a compound annual rate of 30.9% between March 2020 and June 2022.

Regaining the trust of customers was just one step toward changing the fortunes of the bank. Prashant had to do much more than that.

In 2019, the company had around 25% exposure to the infrastructure sector, which is known to be a bit shaky. Most of these loans were NBFCs and real estate companies which struggled due to the slowdown and due to that, the bank's NPAs started rising.

After he took over, he focused on two things cleaning up the balance sheet and recovering cash from stressed assets.

The bank raised Rs 15,000 crore in a follow-on public offer under his leadership in July 2020. Through the capital, the bank was able to grow despite the pandemic.

The company recovered made cash recoveries and upgrades of Rs. 7,290 crore in FY 2021-22.

Due to his efforts, the toxic loans of the company were reduced and its GNPA and NNPA stood at 13.4% and 4.2% respectively in Q1 FY23.

The GNPA and NNPA of the bank stood at 16.41% and 5.03% in FY20.

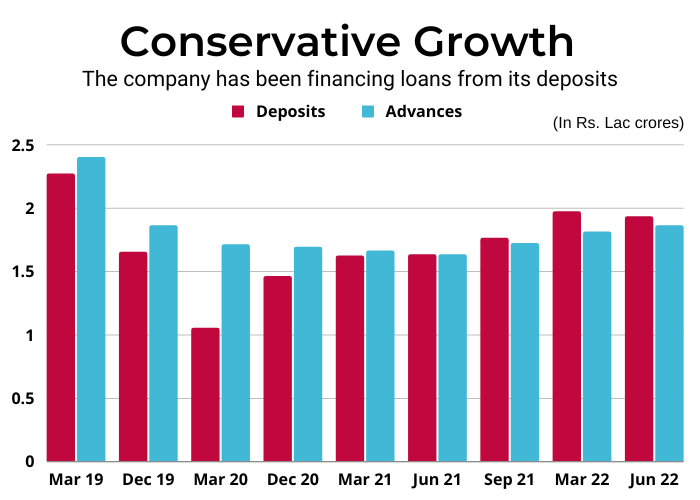

On the advances side, the company is focusing on lending to individuals than corporates. Corporate loans carry much higher risks than retail loans and due to that, the company has been working on changing its retail to wholesale mix. The company aimed to achieve a 60:40 of retail to wholesale loans, in FY23 the company achieved the target and had a loan mix of 62:38.

The advances of the bank grew 14% YOY in June 22. In the two years, its advances have grown at a CAGR of 4%.

Well, the numbers do reflect a positive change in the business of Yes Bank. The company in the next few months would will start selling all of its NPA accounts to an asset reconstruction company, or ARC, where it will hold a minority stake in.

Selling off the loans to ARC would free up the capital of the bank and it would be able to lend more.

It seems like the bank is working to change its fortunes, is it on its way to making a comeback? May be, May be not!

Has it done enough to gain the trust of investors, who lost millions by investing in the company? You tell us! Because you see doodh ka jala b phuk phuk kar peeta hai!

Indian Stock Market Related Articles

List Of Maharatna Companies In India

Sensex Hits 80K: 3 Key Steps Investors Should Take Now

Why Quant Mutual Funds Are Outperforming?

NSE's 90% Cap on SME IPO Listing Prices

How AI Will Shape the Future of the Financial Sector

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing. For detailed disclaimer please Click here.